Money Management

We’ve made it to the end of Financial Literacy Month! Now we’re asking you to spend the next month working on your financial life. Using all the tips you’ve learned throughout April, how many of these money goals do you think you can achieve?

Step One: Committing to Change

It’s simple. The first step to a better financial future for you and your family is commitment. Start by examining your philosophy about money management. Be prepared to take responsibility over your finances and watch as the benefits roll in.

Step Two: Assessing Your Finances

The second step is to determine your financial situation. What are the areas of your life that are financially thriving? What are the areas that could use more attention? This is a broad assessment of your finances. We’ll get into more detailed expense tracking later.

Step Three: Organizing Your Financial House

Now here is where we start to get technical! It is absolutely essential that you be an organized and diligent bookkeeper of your personal finances. Start by collecting all necessary financial information like debts, mortgages, car payments, loans, investments, etc. Anything that brings money in or sends money out, you want to document it for an accurate picture of your financial status. Organization is key!

Step Four: Cleaning Your Financial House

Get copies of your credit report from all three major credit bureaus: Equifax, Experian and TransUnion. To get your free report, simply visit annualcreditreport.com. Consumers get one free credit report from each agency annually. Once you receive your reports, review them for errors and fraud. You can dispute any inaccuracies directly with the bureaus and potentially increase your score by doing so.

Step Five: Calculating Your Net Worth

Financial education isn’t just for those with large net worths. If you have an income you can calculate your own net worth too. All you need to do is compare what you owe (liabilities) and what you own (assets). For example, if you own your car, that would be an asset, and if you pay student loans or other kinds of debts, those would be your liabilities. Now that you have an honest assessment of your current financial standing and know your net worth, you can begin to dive deeper into your finances.

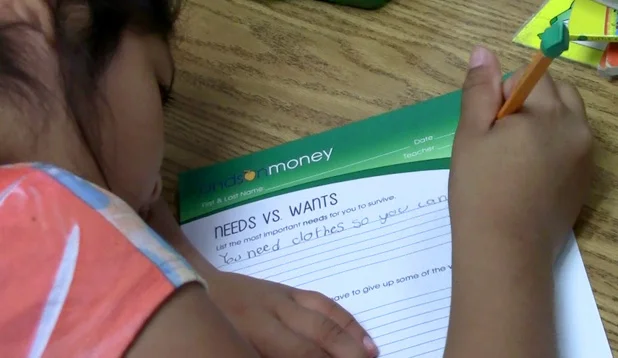

Step Six: Needs vs. Wants

Make a list. What do you NEED to pay for no matter what? Food, housing, clothing, health care, transportation, are some of the most common needs. What do you WANT? Things that aren’t required for you in your daily life like jewelry, entertainment, nonessential commercial goods, and so on. Once you have your list you can start budgeting!

Step Seven: Track and Reduce Your Spending

If you haven’t been already, you need to start a spreadsheet or other tracking method for your spending. This helps you quickly and easily identify where your money is going and where you can afford to spend less. There are three kinds of expenses you can separate your spending into . . .

1) Fixed expenses: which stay the same every month, like rent or car payments.

2) Periodic expenses: these expenses are not always the same amount, and do not occur regularly. An example of a periodic expense would be things like vacations.

3) Variable expenses: groceries, clothes, gas, etc. Items that fluctuate individually in price and varies each time you purchase said product or service.

Once you have your beautifully organized expense sheet, you can start targeting areas where you might be able to save money. Fixed expenses are the most difficult to change, so focus on your periodic and variable expenses. Could you vacation during the off season and travel more affordably? Can you shop at consignment and thrift stores to get your wardrobe at a discount? Be honest with yourself about where you can cut back in your expenses and then start doing it!

Step Eight: Budgeting and Setting Financial Goals

No one wants to give up their daily coffee order or skip a vacation, so don’t think about budgeting as a punishment. One way to budget is by setting financial goals. So instead of thinking about what you’re losing (that delicious oat milk chai latte from your local cafe), focus on what you will gain by putting that saved money towards your financial goals.

When budgeting and setting goals you need to determine the specific cost of your goal and a desired target date. What is something you've been wanting for a long time? Do you want to go on a nice, long vacation this year? Do you want to pay off all your credit card debt? Do you want new patio furniture for your house? The target is up to you, and you can always save for more than one goal at a time, but we recommend starting with an attainable short-term goal first to get started.

Step Nine: Pay Down Your Debts

If you remember one of our earlier posts this month we talked about debt management. There are two popular methods that people use to pay off debt. The first is to pay off the debt with the smallest balance, and then keep moving to the next smallest debt until all debts are paid off.

The second popular method is to repay the debt with the highest interest rate. This method will save you the most in interest charges over time. Choose whichever option is best for your personal financial situation and makes the most sense. Remember you can always change strategies if your circumstances change.

Step Ten: Plan for Emergencies

An essential part of your financial goals should be saving for emergencies. It is recommended to have three to six months living expenses saved in case of emergencies like job loss, economic downturn, or any unforeseen incident that would cause you a significant financial burden.

Now that you have begun to adapt these changes into your financial routines, you have the skills and knowledge necessary to ensure a successful financial future.

Knowing Your Stuff - Money Edition

By Hannah Moore

How financially literate do you think you are in comparison to the rest of the general American public? Take this simple yet revealing quiz to find out. Don't feel bad if you fall short. Statistically, most people do. Even folks with a post secondary education do. The numbers show that 55.7% of Americans with college degrees answered at least one of the three questions incorrectly. The point of this quiz isn't directly about being right or wrong though - it's about how the results reflect what's not known on average, even when it arguably should be. And if that is telling of anything, it's that financial literacy has to be sought after, because it's not usually readily available to the masses. At Andson we aim to make this knowledge readily available for students and their families, because knowing how to handle your money is essential for every age and life situation. We teach these concepts through classroom worksheets, homework assignments, and take home reviews to explain to parents what is being taught and how they can assist in the learning process. Andson curriculum strives for not only a 3 out of 3 score on this quiz, but a more prepared generation of Southern Nevada.

Most Americans Fail This Simple 3-Question Financial Quiz. Can You Pass It?

What's Your Budget Black Hole?

For teenagers or just anyone in general, it’s always extremely difficult to save money. Sure, it’s easy to talk about it or learn about it in class and think it’s a good idea.

But actually doing it? That’s a completely different story.

We are very impulsive creatures and there are all sorts of reasons why we spend money without thinking about it, or without caring at the moment about the consequences of it.

It’s so easy to spend money to “fix” a bad day, or a bad mood, or just to distract yourself from reality for awhile.

When you realize you've run out of money, you may regret your decision. The knot in your stomach begins to tighten.

I’m sure you’ve all heard of black holes.

But did you know that black holes and budgets go hand in hand?

According to the blog Budgets are $exy, “According to NASA, some of the hallmark characteristics of black holes are invisibility and varying size. They literally can’t be seen, and can be sized anywhere from a puddle to a sea.”

If you're having difficulty sticking to a budget, or saving your money, you may be unaware of your budgeting black holes!

So that’s where it all goes!

No, there’s not really a black hole in your wallet, pulling your money into another universe! You are the one sucking it out, and most of the time without even realizing it. That's why it's important to learn how to keep track of your spending.

Budget black holes can be caused by anything! They can be anything from you’re daily latte purchase, to impulsive book buying, to eating out, and taking trips to the movie theater.

They may be areas in which you think you may not spend a lot of money and, therefore, don’t worry about, but they become black holes when they go uncalculated. They add up, and BOOM! Suddenly you’re hit with a reality check. You’re broke!

Once again, the above mentioned blog, http://www.budgetsaresexy.com/2014/01/black-hole-in-your-budget/, says “the key is being able to spot these black holes, and knowing the size of them.”

Therefore, find out what they are and keep track of them to save yourself from the horrors of being broke!

What are your budget black holes?

Find out what they are! PAY ATTENTION to ALL of your purchases, especially the “little” ones! If you find that you’re always broke a few days after pay day, then maybe occasionally skip the coffee or trip to the movies. Don’t give them up, just learn when to put spending off for another few days, making it even better when you do buy something (and you’ll be guilt free)!

College Isn’t Cheap – Fill Out Your FAFSA!

As Sophomores and Juniors, you may hear your Senior friends talking about “FAFSA” a lot. You may figure, “no need to worry, I’ve got years before that.” Then, you wake up. Your parents are freaking out about your college applications, and senioritis is seriously kicking in.

According to https://fafsa.ed.gov/help.htm, “Completing and submitting a Free Application for Federal Student Aid (FAFSA) is the single most important thing you can do to get assistance paying for college.”

You might ask yourself what in the world does this have to do with me?

However, if you are in high school, or are considering going to college or returning to college, this has everything to do with you!

Many students do not know how easy it can be to get money to help with college.

The FAFSA website mentioned above also goes over many fears or myths that students might think would stand in their way when it comes to receiving money for college. These may include thinking that you or your parents make too much money so you won’t qualify for aid, that you have to have good grades to receive aid, that you’re too old for financial aid, or even that the form is too difficult or complicated to fill out.

NONE of these are true!

We already went over why you need it, so let’s go over more specifically what it is.

It is merely a FREE application for federal student aid that can come in different forms including: federal grants, loans, and work-study.

See how easy it is to be walked through the application process and have all your questions answered. Visit the above mentioned website - https://fafsa.ed.gov/help.htm.

Also, be sure to check out this awesome website https://getschooled.com/fafsa-resources.

This website, Get Schooled, has tons of helpful tips and links from not only the experts, but also students like you.

Their topics include:

- Finding out which parent to use for the FAFSA

- Getting an estimate on your aid package

- All of the different types of aid that you might qualify for

- FAFSA tips from your peers

- FAFSA on Twitter, Facebook, and YouTube

Go check it out! It’s not scary at all.

Financial Literacy Update

With the new school year off and running, it's time to shift Andson's gears back into our Financial Literacy Programming.

The Piggy Bank Project at Bracken Elementary School enters its second year and the Andson team will be back in the classrooms delivering financial literacy lessons. New this year, there will be four tiered curriculums differentiated by grades and age groups - this is another example of Andson's flexibility and adaptability to the needs of our students. In tune with this philosophy, Andson has also developed a web-based school banking application that will simplify deposit tracking and reporting.

Promoting financial literacy at an early age will now become a reality in Comal County, Texas. As part of a pilot program for 4th graders, the five-lesson curriculum developed by Andson will be used at 18 different schools and will teach 1,500 fourth grade students the basics of personal finance. Andson is eager to share our passion and expertise with other communities and school districts.

Financial literacy lessons will also continue at Chaparral and Desert Oasis High Schools. Once again, Andson will be tailoring the lessons based on the socio-economic needs of the students and aiming to build mentoring relationships. We are excited for these locations, as well as adding new sites and partners for our High School curriculums this year.

Financial Literacy is at the heart of this organization. This summer was a very special time for us as we were awarded the Pinnacle Award by Treasurer Kate Marshall. Andson was one of three in Nevada to achieve this prestigious award!

Savvy Shopper's Corner! The Smart Online Shopper

Shopping online is a great convenience, yet there is the agony of waiting for your order to be shipped and arrive on time. Here is some information, which may be considered helpful when shopping online. Plan Your Purchase

The earlier you make your purchases, the greater chance they will arrive on time. To cut down on shipping costs, try to order many items at once from a single retailer. Your purchases should be lumped together into one large package with one shipping fee attached. By registering with an online retail site, you can start your online shopping and any items in your shopping cart will be retained until you either delete or purchase them. Then, you can ship everything at once and at one price. Many online retailers offer free shipping on purchases over a certain dollar amount, and online coupon sites regularly offer free shipping coupon codes. If you can’t catch a break on shipping, ordering early enough will allow you to choose standard shipping. It’s always the slowest method, but if you order early, it should get to you on time. Give yourself a little more time if you are ordering from a third party vendor through a big online retailer.

Bargain Hunting

Online shopping presents consumers with a wonderful new advantage – the ease of bargain hunting. Prior to shopping via the internet, finding the lowest price for an item meant using catalogs and circulars, traveling from store to store. Not so much anymore. Often, a simple Google search of the item you want will find even better deals. Search discount sites for the item you want before buying it elsewhere. These retailers purchase excess items that manufacturers could not unload on other retailers at a discount and generally pass the savings onto customers. Don’t be afraid of purchasing refurbished items either—this is often more surplus inventory. Do a quick search for coupons for the retailer available on other sites. Many stores will happily provide you with their own promotional codes if you sign up for their email newsletters. Enter the code before you check out to earn the savings on your purchase.

Return Item Fee

Online shopping could eventually mean not so many physical retail stores, but even if that happens, the warehouse will always be there to storage merchandise and to employ people to stock these warehouses. If you return an item, it still has to be repackaged and replaced, although the retailer has not made any money from the return. As a result, online retailers have begun to charge restocking fees on returned items. Before proceeding to checkout, familiarize yourself with the retailer’s return policies. Simply packaged items like books or defective products should not cost you any more money to return.

Be Secure

There are some measures online shoppers can take to minimize their risk. First, ensure that all online shopping is carried out only on secured sites. It is advisable only to use credit cards rather than debit cards, for online shopping. Credit cards are an extension of credit while debit cards withdraw directly from your bank account. Once in possession of your banking information, hackers can do much more damage to your finances than with your credit card number. Using only one credit card for online shopping is another great way to shop on line. The potential for fraud is limited to one account.

Remember, online shopping, while convenient, could pose more risk.

600 Desert Oasis High School Seniors' Debt Workshop

Desert Oasis Highschool, Check.Andson lesson built on Debt, Check. 600 High Schoolers, Check (gulp). 1 Day. (Wow!)

We had the opportunity April 23rd to teach 6 sessions to Desert Oasis Seniors on Debt, Credit, and Creative Funding of College education.

While this was a bit different for Andson, it was an awesome day! Not only were students informed on the concept of interest rates, predatory lending, and to "think outside the box" in regards to funding college, but we also had 5 individual students looking for mentoring relationships through our program.

This was one of those days that put a smile on our faces - not only can we make a positive impact on so many students in one day, we can engage with a handful of students to achieve short-term and long-term goals through budgeting and planning.

Here is the lesson we taught:

Thanks to Desert Oasis for having us. Word is, they want our whole course for seniors next year.

Pampas is supporting our fundraising efforts on 4/25/13

- Download Flyer -

For the serious steak lovers, Pampas Churrascaria is hosting a fundraiser in support of the Andson Organization. Now through Thursday, April 25, locals and tourists have a chance to accomplish three things at once:

1. Enjoy an unlimited parade of top sirloin, lamb, picanha, smoked ham, shrimp, salmon and much more, all hand-carved tableside, along with an extensive all you can eat buffet bar!

2. Support Andson's academic after-school programs – every dollar counts, and will go directly toward helping our Homework Help & Tutoring Program.

3. Participate in Nevada's Big Give – Pampas will make a final online donation on April 25th that will count towards Nevada's big goal.

Dine out and give back – that’s Fullanthropy! ... vegetarians can join us as well.

- Download Flyer -

Savvy Shopper's Corner! Some Tips For Smart Shopping!

Here are a few helpful tips to cut back on excess spending when shopping at the supermarket.

1. Make a list! It only takes a few minutes to prepare but it will save you from wandering down the aisles and prevent you from shopping for unnecessary items.

2. Substitute supermarket brands for brand name products. You can save on generic, non-perishable snacks, cleaning products, paper goods, and diapers. If you are used to brand name goods, try swapping one or two items to start. Even switching a few items on your shopping list will help you keep more money in your pocket.

3. Buy ingredients rather than prepared products. If you have time to make your own pasta salad at home, you can save money by preparing it yourself versus buying it pre-made at the store.

4. Convenience is costly! Buying fruits and vegetables and cutting them yourself is cheaper than buying pre-cut fruits and vegetables that cost double the price.

5. Learn to buy in-bulk! Buying larger boxes of cereals, crackers, and snacks will last longer. Stock up on items on sale that you use often and store in pantry with early expiration dates in front.

6. Using store and manufacturer coupons can also reduce your total costs at the checkout.

7. Buy a filter for your tap water! It will be more cost effective than buying bottled water.

Never too early to teach children financial resposibility

As we continue to focus our efforts on behavioral finance, we like sharing stories that are worth reading and can help us put into perspective the real challenge of financial literacy. The following article, written as a letter to parents, not only provides insight on how to teach children financial responsibility at various ages, but it also reiterates the importance of early education and parent engagement. Parents and culture will definitely influence the way children understand money and the habits they will develop and continue into adulthood.

Dear Parents,

The long-term key to improving America's overall financial literacy quotient is to get to the kids. What's important is to establish good financial behaviors early because those behaviors will carry over to adulthood. As a father of four, and grandfather of nine, I've seen it work firsthand. Start early, insist on consistency in behaviors, and set a good example. Monitor your saver's progress and celebrate the successes. With that mantra, here's how to get started:

When kids can walk, it's time to start saving. Establish the first behavior of saving by teaching your child to drop coins in a piggy bank or a jar. Explain the meaning of the word save.

Show the money. Periodically, show the child that consistent saving adds up by regularly tallying up your savings.

Take it to the bank. Make a ceremony of taking the child to the bank to deposit the jar of money. Teach them that the bank will give them money (interest) to "store their money."

If there is an allowance, it's time to budget by putting savings first. No matter what the size of the allowance is, break it down between what they can spend, and what they have to save. Note: this may be your first financial "negotiation" with your child - start with saving 50%, and settle for 25%.

The first large purchase. As your child ages, he or she will inevitably want to spend their entire savings - on one item. The answer is "no." Modify budget into more line items - discretionary spending, mandatory saving, and "saving for the large item." This is where the behavior of "buying within means" is established.

"But, I want it now..." This may be the time to develop a new financial concept - borrowing money. That's okay as long as the rules are set, and the "borrower" adheres to them. This is where the behavior of "borrowing within means" is established.

"Can I have a credit card?" Response: No, it's too early. We're sticking to the plan above. However, let me teach you about credit cards - after the "eye roll," stick to your game plan.

"My friends have credit and debit cards." Response: I'm happy for them. We're sticking to our financial plan, and here's why. In my own experience, my children were grateful for instilling financial responsibility at a young age. Start early, consistency, monitor progress, and celebrate success - I'm convinced that's the formula for increasing America's financial literacy quotient many times over. Get to the kids.

Proud Grandfather, Carl George, CPA

Note: This letter first appeared as an e-Wealth Coach article from America Saves. Carl George is the Senior Executive Partner at Clifton Gunderson LLP, a national CPA firm; past Chairman of the National CPA Financial Literacy Commission of the AICPA, www.360financialliteracy.org and www.feedthepig.org; and the proud grandfather of 9.

Education + Personal Finance are the foundation of Andson's April workshops

Andson is constantly committed to teaching students Personal Finance skills. It's April! That means it's Financial Literacy MONTH! We have identified a few key areas that we can really have an impact for students in just one short lesson. Education is an investment that students NEED to make - whether trade school or college, students with a secondary education will have more opportunities than those who only graduate high school. So how can we make sure students have a foundation to understand that debt can hurt a student fresh-out-of-school faster than any other force?

In April, Andson's Financial Team will work with the following institutions to inform students about the pitfalls and positives of credit - as well as provide ongoing support to these student bodies.

- Desert Oasis High School - Seniors will go through an intense Debt and Financial Aid seminar on 4/23. We will be working with over 600 students!

- Nevada Partnership for Homeless Youth ⁃ Nevada has a serious issue with teens that are homeless. However, given the right resources, they can go on to be successful. These students, more than any other, need to be made aware of the resources they can use to fuel their mission of independence and success.

- Nevada State College is an amazing school in the southeast of Henderson. NSC and Andson are partners in so many activities, so it seemed only natural to bring a seminar on pitfall and installment credit to their student body. We are so happy to provide this as a resource to students in Southern Nevada.

We are so proud to be a part of Southern Nevada - let's give our students the resources they need to succeed!

Behavioral Finance and Andson - worksheets alone don't work

A statistics professor in my MBA program made a statement on the first day of class, "I can train you how to be a $10 calculator, or I can train you how to think." Obviously, gone are the days of living without smart phones, auto-correct and calculators.

So why are we still teaching personal finance as textbook terms and definitions? Why are we spending time on the things that students will inevitably forget; more importantly the things that they can easily look up on their phones? (Please Note: We do worry about many students' capability to spell and do simple math, but that's why we created Andson Academics).

We need to teach them that knowledge equals power. When faced with questions about IRA accounts, APRs or the details of an annuity, do some research on Google, instead of believing the salesman. We need to be able to instill that delayed gratification and PYF (pay yourself first) gives them spending choices and spending power.

Behavioral Finance is the term that is gaining ever-so-much momentum right now in this field. That is, instead of teaching a student about textbook definitions, let's teach them how to think about finance.

- What should I be leery of?

- When does an interest rate raise a red-flag?

- What are the fees that will be involved?

- Where can I go for help outside of a payday loan?

All of these are examples of teaching young people how to think about their money. Time Business & Money has a great article right now on the concept of changing behaviors instead of just teaching facts. We couldn't agree more and in fact pride ourselves and our programs on providing more than just a workbook or worksheet.

Roth, who runs the infamous blog Get Rich Slowly admits that he himself learned all the "basic financial literacy," in his senior year of high school, but was no better because of it.

Roth goes on to say that personal finance is something internal for most people - though for many there is definitely a cycle of poverty they need to overcome. What needs to be taught is that in order to make a change, it needs to happen within us. Otherwise it's just like a fad diet - you always end up back at square one.

I myself cannot begin to count the amount of times that we see young people that just don't want to end up in the same debtor situations they've seen friends or family end up in. Many times that's enough and it works. More often than not though, one is the sum of their surroundings; so bringing a fresh way of thinking and perspective into the classroom is more important than ever.

Let's continue with a mission to change behavior in our students, and not just make them calculators and dictionaries when it comes to personal finance.

Sources:

Time Business & Money

http://business.time.com/2013/03/11/why-financial-literacy-fails/

JD Roth

http://business.time.com/author/jdroth/

Get Rich Slowly

Helpful Tips to Paying off Your Student Loan

When it comes to college, most people find the biggest struggle is being able to pay for it. Some people do not even go to college because of high tuition and other extra costs like books and parking passes. It seems almost impossible to attend college without having to take out a student loan. But once school is over and you get your degree, student loans are dropped on you and it is up to you whether or not you will successfully pay them off. People are defaulting more than ever because of the unexpected high monthly payments. People do not consider the interest of a loan, how long it will actually take to pay it off, or that maybe their career will not be as successful as planned. The best way to avoid the unexpected feeling and stress of student loans is planning. The sooner you start planning for college and researching different types of tuition plans, the more control you will have of your future. You never want to accept the first plan that a person hands you. Researching and talking to advisors will help you decide. Advisors can be anyone from a financial advisor to a friend that you trust.

Be prepared to start paying off your student loan as soon as possible. A big way to put a dent into your student loans is to pay more than the minimum payments. Even an extra $20 can make a difference. The extra $20 can come from budgeting your money properly.

These are just a few helpful tips for you but there are several different ways to help you with your student loans. Again, planning is key! Prepare yourself for a more successful future!

To obtain more information, read:

http://finance.yahoo.com/news/6-tips-paying-off-student-132815610.html